OUTLOOK SUMMARY

- The US recovery is slow going—more true of GDP than jobs—but new developments point to faster growth in 2013, once the disruptions from payroll tax hikes and sequester cuts pass. That expectation (not the Fed’s actions) surely is what has powered the stock market into record territory.

- The Cyprus crisis underscored (yet again) the community’s resolve to stay the course and move toward further economic integration. And the Bank of Japan’s aggressive move to boost its economy is a hopeful sign for global activity.

- In the US, the real estate sector is poised to breath new energy into the recovery. And the rebound in business capital investment is keeping this forward-looking activity on a recovery-like trajectory.

- Claims that there is no recovery, that the economy is caught in a debt trap, and that the stock market is being inflated by the Fed’s “printing press” belie the obvious signs of recovery, miss the meaning of all-time-record profit margins, ignore the correction of real estate excesses, and fail to understand that the Fed’s asset purchases have nothing to do with monetizing debt, liquidity, or money.

OUTLOOK. SUNRISE IN AMERICA

SUMMARY

The shackles related to the real estate excesses of the last decade that have been restraining the pace of the US economic recovery are quickly falling away and freeing the economy to pick up speed gradually to a pace that is more common for a recovery. The growth pace is forecast to quicken this year to at least 3 percent over the four quarters of the year, surpassing the 2 percent growth pace so far in the recovery since 2009. Growth should be even faster than that for the next several years, reaching speeds of 3.5 to 4.0 percent. Fiscal policy will provide no support for the balance of this year, because the massive stimulus that was put in place to cushion the economy in the 2008 and 2009 recession has been winding down since 2011 as planned and the sequestration agreement is restraining spending growth this year. With the recovery slow and unemployment high, periodic growth disappointments naturally lead to collective “shivers”, even when transitory factors are known to blame. Still, the economy’s foundation is solid and the recovery is not fragile.

Many of the jobs lost during the recession have been recovered or replaced. Still, much more growth is needed to restore the economy to full health. Real GDP presently lies about 7 to 10 percent below potential output, so the economy will need to grow faster than trend for a while to achieve the Federal Reserve’s congressional mandates of maximum employment and stable 2 percent inflation.

Job trends best frame the challenges. Businesses have recovered or replaced roughly two-thirds of the jobs that were lost during the downturn. Employment in many states is back to where it was before the recession or higher. Others are lagging. But all are recovering to one degree or the other. Even in California, which has been held back by severe real estate excesses, employment has recovered 55 percent of the jobs lost during the recession. Despite all this, the progress to date has created only one-third of the jobs needed to return the economy to full employment. Full employment goal posts are continually moving forward, with the underlying labor force growing about 1½ million annually. Today’s labor force is 2 percent larger than in 2007 and much more than that including those under 55 years of age who temporarily dropped out.

The under-employed state of the US economy has pulled annual inflation down to 1¼ percent, a rate that is well below the Federal Reserve’s 2 percent long-run inflation target. That inflation metric refers to the chain price index for personal consumption expenditures the FOMC targets.

With official unemployment still far too high, even ignoring the discouraged dropouts, and inflation too low, the Fed says it will leave its stimulative policies in place until more recovery progress is made. So, long-term interest rates likely will remain unusually low for the balance of this year and the next. In contrast to what usually occurs when the Fed normalizes its policy, the yield curve could steepen further and remain steep. As the case for large scale asset purchases wanes, long-term interest rates likely will climb back to more normal levels. In that event, the Fed will be quite cautious until it is satisfied that the economy can absorb the expected backup in long-term rates.

Equity investors seem increasingly confident about in the economy’s prospects. The Wilshire 5000 index of all publicly traded stocks broke the October 9, 2007 record on January 25, 2013. The better-known Dow Jones Industrial Average and S&P 500 indexes followed suit last month.

With the economy still in the early days of recovery, many assume that the stock market’s rise to record highs must be artificial, inflated by the Federal Reserve’s “easy money policies”. The artificially low rates engineered by the Fed certainly are “inviting” investors to move funds from cash to longer duration assets. Still, investors would not buy stocks if the economy were not convincingly on the mend. And equity market participants tend to anticipate future developments long before they are obvious to the general public.

In fact, claims that markets are up only because the Fed is printing money reflect a fundamental confusion about Fed policy and money creation. The claims would make sense if the Fed were actually expanding liquidity and monetizing debt. But that’s not what the Fed is doing. Claims that the Fed is flooding markets with cheap money is a knee-jerk reaction to a poor memory of a flawed or obsolete lesson from standard Money & Banking textbooks. The Fed’s asset purchases have no impact on liquidity or on the money stock, because the reserves it creates accumulate only as excess reserves. The Fed’s policies are not boosting liquidity. Instead, they are depressing long-term interest rates which is incentivizing investors to move funds from cash to risk assets, a trend that shifts liquidity from one asset class to another but does nothing to add to liquidity.

Claims that the Fed’s policies are pumping up the stock market would made sense if business profits, the “North Star” for investors, were not at a record high share of GDP. In addition the real estate excesses that have restrained the economy’s recovery pace have largely vanished. The leverage that built up amid the severe real estate speculation in the last decade has come down significantly and debt service of households is at the lowest level in relation to income since 1979 when the Fed began to track debt service trends. The near-term outlook for tax policies is a bit clearer in the wake of the American Taxpayer Relief Act of 2012 that made permanent most of the 2001 and 2003 tax cuts. And political conversations about the nation’s fiscal challenges finally are beginning to acknowledge what insiders have long known, that the principal fiscal challenge centers around the growing structural imbalance driven by federal healthcare spending. Today’s budget deficits are mostly collateral damage related to the recession. That’s why the deficit now is shrinking (see Appendix 3 on page 21). And layoffs are almost back down to pre-recession levels.

Two more silver linings appeared recently on the global outlook. The reluctance to push tiny Cyprus out of the monetary union, following its banking crisis, underscores the resolve of the European effort to move forward on the path of economic integration. Second, the Bank of Japan’s decision to take much stronger actions to boost its stagnant economy and drive its inflation up from the current zero per cent level, promises to end a decade of economic stagnation and provide helpful support for the global economy.

1994 IS NOT THE TEMPLATE

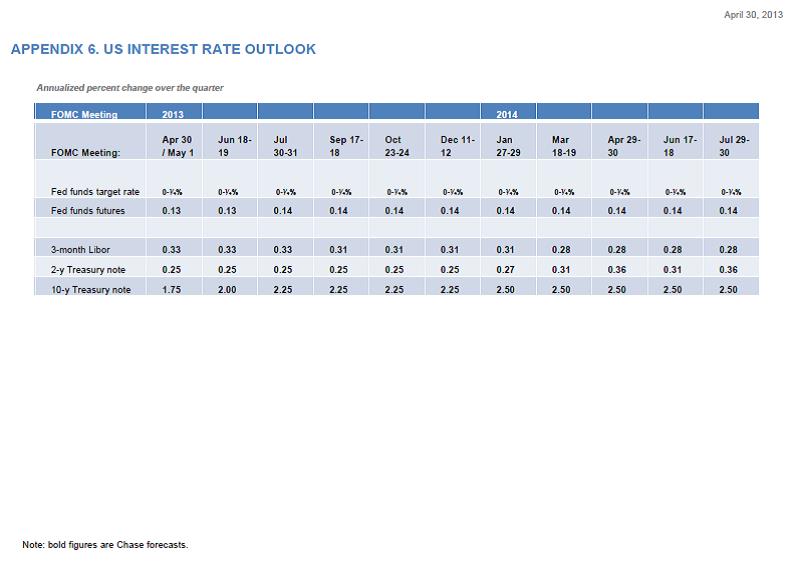

The Federal Reserve has forced all interest rates below equilibrium levels. Overnight rates, the Fed’s traditional monetary tool, are close to zero. Longer-term Treasury yields are about zero in real terms, far below the more normal 2 to 3 percent level, because the Fed has removed $2 to $3 trillion of securities from the market with large scale asset purchases (Outcome-Based Purchases, as they are now called). As the economy improves and the Fed terminate its asset purchases and then shrinks its bloated balance sheet, interest rates likely will climb back up to more normal levels.

With that prospect looming, as the economy moves forward, many worry (quite a few predict) that the eventual interest rate adjustments will be turbulent. Some predict a repeat of the 1994 experience, when global bond markets sold off sharply as the Fed began to tighten policy. Of course, the 1994 experience was followed by the benign bond market developments that accompanied the Federal Reserve’s tightening – actually, normalization—of interest rates. Recall Alan Greenspan’s bond market “conundrum” at the time, a reference to the tepid rise in bond yields even as the Fed began to lift its short-term interest rate target.

Why did the Fed’s tightening in 1994 create so much turbulence and are there any lessons in from that moment that apply to the current circumstances? Analysts at the Federal Reserve Bank of New York recently published a blog that examined the behavior of interest rates during periods of Fed tightening that shed some light on the events of 1994. They looked at the behavior of interest rates, decomposing them into a path of the evolution of expected short-term interest rates and a term premium, the theoretical compensation investors demand for the risk that the expected path of interest rates implied in interest rates might be wrong. They claim—and admittedly the answer depends on estimates of the term premium—that the reason why interest rates rose so much in 1994 was because market expectations of the path of short-term interest rates were too aggressive and that the term premium did not behave all that unusually.

Their assertion will resonate with many who remember the events of the time. The Fed’s response may have contributed to the 1994 bond market turbulence. Recall that the Fed began to tighten policy in small steps. It stuck to the slow but steady pace until the fall, when it accelerated the pace of tightening and moved in increasingly bigger steps. Moreover, in the background, there was a strongly held view that the economy’s noninflationary unemployment level was about 6 percent. Unemployment was fast approaching that level at the time. As the unemployment rate eventually fell to 4 percent without spurring inflation, estimates of the noninflationary unemployment rate came down.

What about now? Two themes strongly imply that when the Fed normalizes its policies, the process will be cautious and gradual. First, for all the progress on unemployment and employment—and the steady decline in weekly jobless claims illustrated on page 7 confirms that the job market is improving—the job market still is only in the early innings of recovery, taking account of hidden unemployment. The figure on page 8 illustrates how the full employment goals posts are moving downfield and why it is that, despite two thirds of the job losses in 2008 and 2009 now recovered, the level of employment needed to reach full employment is higher than it was in 2007. The figure on the previous page also indicates why the official measure of unemployment may only represent half the true level of unemployment.

Inflation represents the other striking difference in the current environment compared with 1994. Inflation currently lies below the Fed’s long-run target; in 1994 inflation was about 3 percent and was thought to be still too high. If inflation remains below the Fed’s goal, the expected normalization of Fed policy will come slowly, in contrast to 1994.

So yes, bond yields are artificially low. Most market participants understand that. So, rates will back up when the Fed begins to normalize its policy rates. But the adjustment likely will be orderly and gradual, because the economic recovery will be gradual.

US FISCAL SUPPORTS PULLING OUT

The shift in fiscal policy from implementing then unwinding stimulus has retarded US growth since 2010. Fiscal policy probably will remain a headwind for the balance of this year. Elevated spending by countercyclical programs and additional stimulus initiatives cushioned the 2008 and 2009 recession but that support has been pulled back for the past two and a half years—government spending is falling as a ratio to GDP.

The fiscal impact is illustrated in the figure on this page. Although real GDP has been growing at only a 2 percent annual pace for the past four years of economic recovery, real GDP excluding the spending of the public sector—and this excludes the support and then withdrawal of tax relief—has been expanding 3.0 to 3.5 percent annually since 2010.

The drag from the government sector was expected to ease this year, but automatic spending restraint related to sequester agreement seems likely to extend the fiscal drag this year.

A NEW DAY

Brightening economic prospects in three sectors in particular this year are likely to breath new energy into the US economic recovery.

Sales of motor vehicles have fully recovered from the 2008-09 collapse that was triggered by the unprecedented credit freeze. Sales are rapidly approaching a 16 million unit annual selling pace that seems to be a steady-state level of purchases. The steady recovery to date, with sales running 15¼ million units, is far better than the 14 million selling pace the industry had been assuming would be reached in 2012. Although that means that there will be little new support coming from a recovery of sales, new support in the industry will come from rotating upstream as the job market and incomes continue to recover.

From the point of view of the economy, it matters little where the vehicles are produced, Canada, the US, or Mexico, because the Nafta economies are highly interconnected. Nonetheless, there is scope for increased production at US-located that manufacturing facilities, perhaps to a 12 million unit production pace from the current 11 million unit pace.

The recovery of credit flows has been a life saver for the motor vehicle industry. That’s because most new car purchases are financed with credit or are lease financed. Favorable developments in subprime car lending is an example of the importance of credit and the benefit of the Federal Reserve’s policies. The exodus of funds from cash to risk assets has reduced the rate demanded for asset backed securities backed by subprime auto loans relative to risk free rates and this has opened the flow of credit even for borrowers whose credit histories are challenging. This is not a sign of new financial excesses, because the rates charged for such loans are less attractive than the rates those with stellar credits face.

The residential real estate sector is seeing more signs of live in virtually all corners of the industry. That’s a promising development, because the sector has until recently been a significant drag on the US economic recovery.

Notably, home builders have worked off most of the glut of new homes built in the last decade. In normal times, 1.5 million to 2.0 million houses are needed each year to accommodate the growth in the number of new households, including those coming from immigration, to replace the 300,000 or so of houses that are torn down or destroyed, and to meet the ever-changing demand for second homes. As the figure on the previous page indicates, builders have been putting up roughly one-third as many new houses as are needed in steady state. That’s been the main reason why the US economic recovery has been so slow. And it is the reason why the glut of houses built during the housing debacle has largely vanished and builder inventories are back to a lean four-month’s-worth-of-sales level of unsold homes.

There are new signs of life in the real estate market as well that will be generating considerable collateral benefits. With house prices back to affordable levels property is beginning to move and prices are rising again. Not only is this easing the severity of the underwater problem but it also encourages homeowners to invest in home improvements. And as underwater properties surface, more homeowners will be able to put their houses on the market if they are so inclined, generating new income by boosting turnover of existing property.

The surge in new home starts (see the figure on page 13) has barely shown up in measure of economic activity like GDP, because the bulk of the value added and new jobs created by housing construction comes as the homes are being built after the hole is dug for the foundation. A full normalization of housing activity likely will lead to the creation of roughly one million additional construction jobs and employment that is indirectly involved in real estate.

The second wind the capital goods industry is catching represents another promising development for the US economic recovery. Business capital goods investment burst out of the gate in 2010 and grew at a double digit rate for a while, as it had in virtually all past economic recoveries (see the figure on this page). But orders for capital goods retreated suddenly last year, sparking worries that uncertainty about the political backdrop might be getting in the way. The slump was short-lived and orders for capital goods have bounced back. This along with the robust backlog of aircraft orders has revived optimism about a key driver of the economic recovery.

The economy’s recovery pace is expected to speed up. From time to time, the recovery pace may seem to lose momentum and indeed, recent economic data have implied that manufacturing activity may be moderating. But the recovery is firmly in place and it is broad based (virtually all state economies are recovering). So, spells of disappointing economic data should not be seen as a sign that the recovery is stalling.

APPENDIX 1. THE JOBS-GDP DISCONNECT

For sure, the US economy’s recovery has been slow. For example, the illustration on the following page, which compares the trends in employment in this expansion with that in other economic recoveries, indicates that employment trends in the last four years (by now, the employment estimates are quite reliable), have lagged behind all of the other economic recoveries in the post-World War II Era. But considering the magnitude of the damage that occurred in this downturn, the $2 to $3 trillion mortgages that are under water, the economic recovery is notable.

The respectable if slower-than-normal job market recovery despite the very slow pace of real GDP growth has led to considerable head scratching. The dichotomy between the jobs recovery and real GDP growth is a significant puzzle because GDP figures tend to shape the public’s perception about the economy’s performance. The National Income estimates tend to be accepted as the indicator of record when it comes to describing the economy’s performance. Nonfarm payroll employment has expanded at a 1.8 percent annual pace since the recovery got underway in the summer of 2009 and the unemployment rate has been falling about one percentage point per year. This is a performance typically associated with much stronger growth—a pace that historically would have been around say 3.5 to 4.0 percent annually. The unprecedented and temporary withdrawal of discouraged job seekers who will return as opportunities open up is part of the answer to the unemployment rate puzzle. And it is possible that slow productivity growth has lowered the bar for new hiring, although downside productivity surprises usually result in a squeeze on business profits that is notably absent.

There’s a third explanation for the relatively strong performance of the job market. Maybe real GDP figures are underestimating the strength of the economic recovery. It’s not hard to believe that: GDP represents an aggregate of all the final spending in the economy and tracking that requires information from far and wide; given the long processing lags, GDP estimates are modified for several years before they are finalized; estimates of GDP during the recent downturn were later revised down substantially over the next three years.

The time-tested Okun’s Law relationship between changes in the unemployment rate and deviations of growth from potential growth can be exploited (reverse engineered) to make inferences about future potential real GDP revisions. There are three moving parts in this relationship, including the noninflationary rate of unemployment, preliminary estimates of actual growth and potential growth. Okun’s Law indicates that deviations in the unemployment rate from the noninflationary rate tend to be about 35 percent in the opposite direction of the difference between actual and potential real GDP growth. Economists at the Federal Reserve Bank of Boston recently published work on this exercise that is very informative. They examine errors in the Okun’s Law relationship that arise using real time (current at the time) estimates of GDP and then they correlate those errors with subsequent revisions to GDP estimates to examine whether the errors give a “heads up” on potential GDP revisions. They conclude that such real-time errors (arising from preliminary GDP estimates) contain significant information about future GDP revisions. GDP estimates prior to five years ago are locked down (will not be revised further in upcoming annual benchmark revisions) but recent GDP estimates are preliminary. For that reason, the Okun’s Law relationship appears fairly consistent over time until recent years. In recent years, however, a significant “error” has opened up in the Okun’s Law relationship between unemployment and economic growth and this is illustrated in the figure on the following page. As the figure illustrates, the actual unemployment rate has been declining at a rate of almost one percentage point annually since 2009. Instead, the unemployment rate would be expected to be rising over the course of this recovery based on the Okun’s Law relationships and an assumption that potential real GDP growth had not slowed significantly.

Conclusion: keep an open mind about the pace of economic growth in this recovery for a couple more years, until the ink is dry on preliminary GDP estimates.

APPENDIX 2. THE BENEFITS OF MARK-TO-MARKET DISCIPLINE

The US economic recovery has been slow by comparison with past recoveries. It could have been worse. Memories of the dark predictions made during the credit crunch may be fading but it is notable that the US economy is recovering far faster than many at the time thought likely. Pessimistic predictions about the US economy, made at the time of the severe correction of house prices, was understandable: plummeting house prices in the aggregate left $2 to $3 trillion of mortgage obligations under water, wiping out that much from household net worth. It was reasonable to forecast that, based on the historical behavior of consumers to balance sheet developments, households would have to curb their spending and significantly raise their saving in order to repair the damage to their financial positions. Even if households saved twice as much as the $500 billion they were saving annually at the time, it was assumed that it might take them the better part of a decade to repair the damage to their balance sheets.

As it turned out, consumer spending has been remarkably robust, taking account of the trends in employment and the real estate sector is on the mend. Saving has gone up only a little, to 5 percent from3 percent. The ratio of household net worth to income has recovered almost 60 percent of the loss in 2008 and early 2009. Debt obligations are at the lowest level they have been relative to income in more than a decade. Debt service is near the lowest it has been since the Federal Reserve began to make such estimates. And the value of assets held by households is back near the all time high in relation to income.

Why has the US economy managed to recovery relatively quickly from the excesses of the housing bubble when the Japanese economy continues to suffer from lingering drags related to its housing excesses so long ago?

The contrast between the US experience and Japan likely has a lot to do with the role of the financial system in the US and mark-to-market discipline. Japan’s bad housing loans were entirely held by its banks. They weren’t securitized. As a result, failing loans eroded bank balance sheets. Japan chose to allow its banks to slowly recover by using their earnings repair the damage. Bank credit could not grow rapidly and its economy recovered slowly.

In the US, most subprime loans and a high percentage of other types of mortgage loans were securitized. When the market belatedly recognized that the correction of speculative house values would drive many mortgages under water and lead to a wave of strategic defaults, the value of the assets backed by underperforming loans plunged, forcing investors to mark-to-market their holdings in recognition of the new reality. That mark-to-market discipline was abrupt and painful, but enabled to US to move forward more quickly than if there had been no securitization.

APPENDIX 3. FEDERAL DEFICIT UPDATE

Federal budget deficits are a concern for good reason. If when the economy returns to full employment the government must compete with private borrowers for credit to finance a deficit, interest rate pressures will mount and many private investment projects will become financially untenable, with negative economic implications.

The cause of a federal deficit is key. A deficit caused by pressures related to a weak economy—that is, a cyclical deficit—generally is benign. Enlarged financing needs of the public sector are offset by reduced private credit needs. Not so in the case of a structural deficit, which exists even when the economy is strong. A strong economy cures a cyclical deficit. Only policy adjustments can cure a structural deficit.

Today’s federal deficit appears to be largely cyclical in character, a result of the severe recession and underemployed economy. The deficit was negligible in 2007 before the recession hit. Pressures on interest rates are minimal. And now the deficit is beginning to shrink and likely will continue to do so as the economy recovers.